Role of AI Solutions in Insurance Fraud Detection

One of the most urgent and painful realities of the insurance industry is that you’re being robbed every year, and so are your customers—often without anyone realizing it until the premiums rise again. Suspicious activities and insurance fraud cost the industry over $308 billion annually in the U.S. alone, according to estimates. This massive financial drain spans auto, health, property, life, workers’ compensation, and more, silently inflating everyone’s costs.

To combat this, one of the most effective approaches is to utilize artificial intelligence or AI-driven insurance software solutions. AI flags suspicious activities early in the claims lifecycle, automates low-risk reviews, prioritizes complex cases for investigators, and even adapts to new fraud strategies through continuous learning—reducing false positives, accelerating legitimate payouts, and preventing losses before they escalate.

In this blog post, we will explore the role of AI solutions in insurance fraud detection and safeguarding both insurers and policyholders.

Why Non-AI Insurance Fraud Detection Methods Fall Short?

Non-AI insurance fraud detection methods, such as manual reviews, reactive, rule-based systems, and basic heuristic checks, despite being effective for years, are falling short today. As fraudulent schemes are now more sophisticated, coordinated, and technology-enabled, resulting in billions in undetected losses, inflated premiums, wasted investigative resources, and eroded trust. Here are the key reasons why non-AI methods struggle so severely:

1. Dependence on static rules

Rule-based systems rely on predefined, static thresholds and “if-then” logic (e.g., flag any claim over $X or with multiple claims in Y days). Fraudsters quickly learn these rules and design schemes to stay just below the radar.

2. High false positive rates

Legitimate claims may be flagged as suspicious simply because they match a predefined rule. Investigators then spend valuable time reviewing cases that ultimately turn out to be genuine.

3. Growing volume and complexity of insurance data

As thousands to millions of policies and claims are processed each year across multiple products, most non-ai methods fail to keep up with the rising number of deepfakes and sophisticated forgeries that look authentic to the human eye or basic checks.

4. Reactive Rather Than Proactive Nature

Non-AI detection is often after-the-fact: fraud is identified only after payment or during slow audits. There’s no real-time prevention or early flagging of suspicious activities during submission or the claims lifecycle.

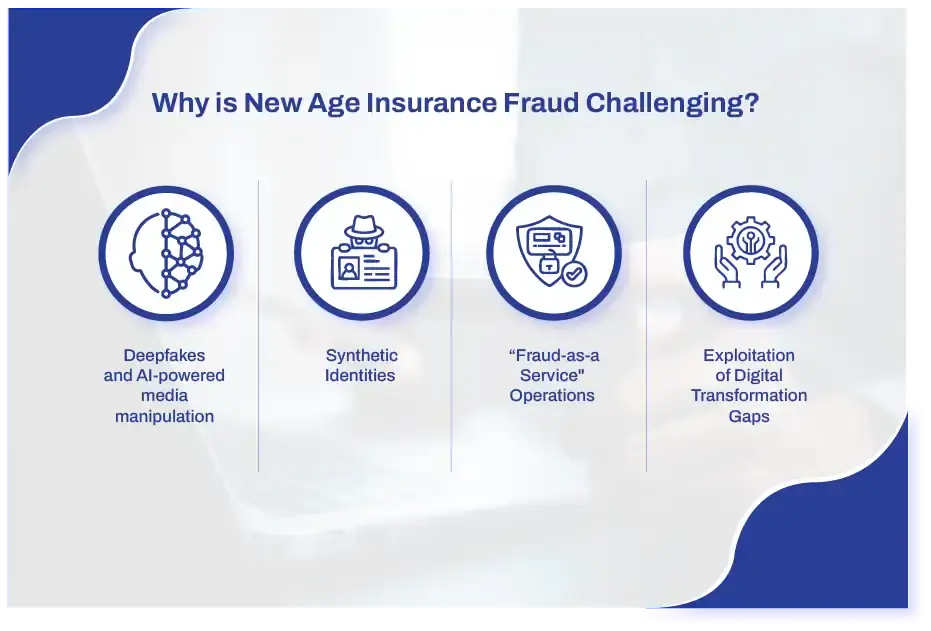

Why is New Age Insurance Fraud Challenging?

In this artificial intelligence (AI) age, not just insurance companies are tech-savvy, but also fraudsters. This is why insurance fraud is mutating at a terrifying pace. Fraudsters armed with generative AI, deepfakes, synthetic identities, and organized “fraud-as-a-service” networks are outpacing traditional defences. Here are the following factors that make these frauds particularly brutal and hard to stop:

1. Deepfakes and AI-powered media manipulation

Freely available generative AI tools are extensively used to create hyper-realistic fake photos, videos, documents, invoices, and even voice clones. Deepfakes impersonate witnesses, fabricate accident footage, alter damage evidence, or simulate medical reports—looking utterly authentic to human eyes or basic checks.

2. Synthetic Identities

Criminals combine stolen real data with AI-generated fakes to build entirely fabricated personas—complete with backstories, social media profiles, documents, and histories—that pass initial verifications.

3.”Fraud-as-a-Service” Operations

This is a new, evolving, underground, subscription-based business model that cybercriminals are selling and using to commit fraud. In these ready-made tools, counterfeit docs, compromised data, bots for small-claim floods, and coordinated staged accidents are performed to commit fraud.

4. Exploitation of Digital Transformation Gaps

As insurers push digitization—mobile apps, instant claims, IoT data—new vectors open: manipulated telematics, fake sensor readings, phishing for policy changes, or AI-altered submissions during onboarding/underwriting.

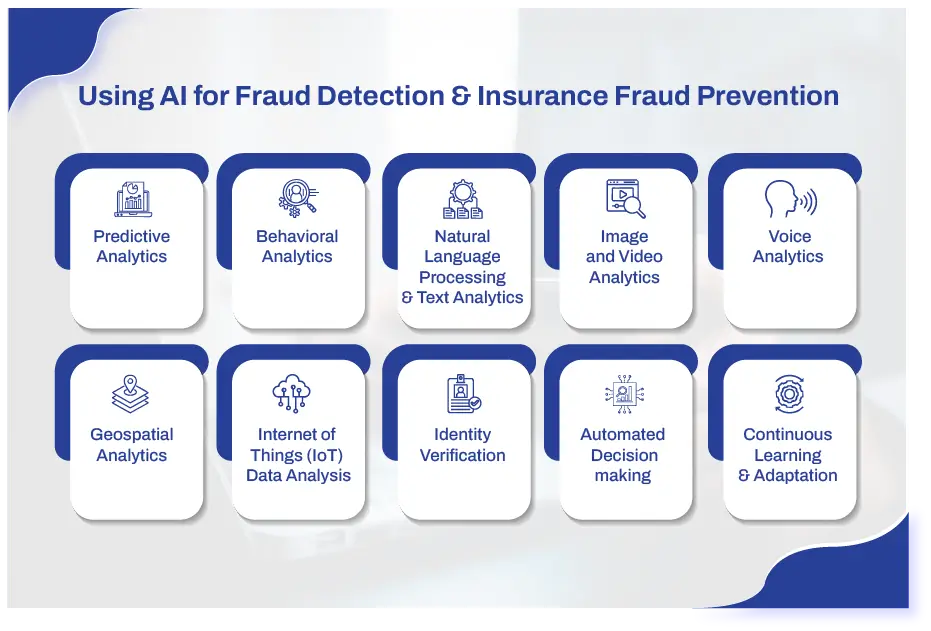

Using AI for Fraud Detection & Insurance Fraud Prevention

On one hand, where AI has been extensively used for committing fraud, organizations are also utilizing it to prevent it, mostly via AI-powered digital insurance solutions distribution partners. These solutions eliminate the limitations faced by traditional insurance systems, boost personalized policies, perform risk analysis, centralize data from multiple sources, and detect, prevent, and eliminate insurance fraud.

This is how insurers, through AI in insurance, detect and prevent fraud:

1.Predictive Analytics

Predictive analytics models analyze historical claims data, policyholder behavior, and fraud patterns to estimate the probability of fraud in new claims. This is how it enables insurers to prioritize high-risk claims for investigation, while they can proceed with genuine claims faster.

2. Behavioral Analytics

Behavioral analytics examines patterns in policyholder and claimant behavior, and promptly identifies any unusual behavior, such as frequent policy changes, repeated claims across different insurers, or suspicious claim timing.

3. Natural Language Processing (NLP) & Text Analytics

AI uses Natural Language Processing (NLP) to analyze text or data. This model can therefore easily identify suspicious language patterns, inconsistencies in claim narratives, or missing information that may indicate potential fraud.

4. Image and Video Analytics

AI models can detect images and videos submitted during the claims and identify any signs of image manipulation, staged damage, or inconsistencies between reported incidents and visual evidence. This model is particularly helpful in auto insurance and property insurance claims where visual verification plays a major role.

5. Voice Analytics

Through speech recognition and voice analytics technologies, AI can analyze recorded conversations between claimants and insurance representatives. This is where it can detect emotional stress signals, inconsistencies in statements, and suspicious speech patterns.

6. Geospatial Analytics

AI uses location data, satellite imagery, and mapping technologies to verify the accuracy of claim information. For example, insurers can confirm whether an accident occurred at the reported location or verify property damage caused by natural disasters using satellite or drone imagery.

7. Internet of Things (IoT) Data Analysis

Connected devices such as vehicle telematics, smart home sensors, and wearable devices provide real-time data that insurers can use to validate claims. For example, vehicle telematics can reconstruct accident scenarios, while smart home devices can verify events like water leaks, fire incidents, or security breaches.

8. Identity Verification

Digital distribution platforms primarily use AI to verify customer identity using biometric authentication, facial recognition, and document verification technologies.

9. Automated Decision-making

AI models assign fraud risk scores to claims based on multiple data signals, enabling insurers to prioritize investigations efficiently.

10. Continuous Learning and Adaptation

AI models are especially gaining popularity due to the fact that they learn and adapt continuously, unlike rule-based systems. In insurance, they learn from new fraud cases, investigation outcomes, and emerging fraud patterns. This enables insurers to adapt quickly to evolving fraud tactics and improve detection accuracy over time.

The Way Forward: Building Fraud-Resilient Insurance Systems with AI

Just as insurance and its distribution are evolving, so too is insurance fraud. Most insurance companies are building insurance portals to automatically process claims and enable self-service, which has led to increased incidences of tactics such as manipulating systems, staging incidents, or exploiting process gaps.

This is where Insurtech and insurance distribution software solutions, combined with AI-driven anti-fraud technologies and advanced data analytics, are strengthening fraud detection in insurance. AI systems can analyze vast volumes of claims data, identify unusual patterns, and flag suspicious transactions in real time. Platforms like Ensurite provide insurers, reinsurers, and insurance distribution partners—including brokers and agents—with intelligent tools that help strengthen fraud detection across the entire distribution and claims ecosystem.

In an industry where billions are lost to fraud each year, adopting resilient and technology-enabled fraud detection systems will be essential for long-term sustainability. If you want to know how Ensurite AI-powered capabilities can help you prevent frauds then get in touch for a free demo.

Explore more Blogs: https://ensurite.solzit.com/blog/

Frequently Asked Questions

How does artificial intelligence help prevent insurance fraud?

Artificial intelligence uses models such as predictive analytics, behavioral analytics, geospatial analytics, text analytics, voice, image, and video analytics, as well as identity verification. All these help it detect any anomalies. For example, AI models can detect unusual claim patterns, repeated claims from related entities, or inconsistencies between reported incidents and available data sources.

What is the future of AI in insurance fraud prevention?

The future of AI in insurance fraud prevention lies in more intelligent, data-driven systems that can continuously learn from new fraud patterns. Emerging technologies such as advanced machine learning models, behavioral analytics, and real-time anomaly detection are expected to play a larger role in identifying fraud across the entire insurance lifecycle

Can AI work alongside human fraud investigators?

Yes, AI is most effective when it works alongside human fraud investigators. For instance,

AI systems are extremely good at analyzing large datasets, identifying patterns, and detecting anomalies that may indicate fraud. However, human investigators bring contextual understanding, industry expertise, and judgment that are essential for confirming fraud cases.

How does predictive analytics reduce insurance fraud risk?

Predictive analytics reduces insurance fraud risk by analyzing historical claims data to identify patterns associated with fraudulent behavior. Machine learning models trained on past fraud cases can evaluate new claims and estimate the likelihood that they may involve suspicious activity.

By identifying high-risk claims early, insurers can focus investigative resources where they are most needed and reduce the chances of fraudulent payouts.

How does AI reduce financial losses caused by insurance fraud?

Fraudulent claims that go undetected can result in significant financial losses for insurers, which ultimately increase costs for policyholders as well. AI can analyze large datasets in real-time and thus can quickly identify unusual claim behavior, detect inconsistencies in claim documentation, and flag anomalies that traditional systems might miss.

As a result, insurers can prevent financial losses, improve operational efficiency, and maintain fair pricing for legitimate policyholders.